BDCs

BDC Common Stocks Market Recap:

Week Ended March 18, 2022

At Long Last

This was a monumental week for the markets as the Fed finally got off the pot – months and months after inflation began to rage to levels unprecedented in a generation – and raised short term rates.

By 0.25%.

More importantly for everyone watching, the Fed sort-of promised to keep raising those rates throughout 2022 and into 2023.

By the end of the year, the Fed Funds rate should be at 2.0% and next year reach 2.75% – the highest level since 2008.

All this was very much expected and signaled well in advance but the major markets – happy for any sort of clarity – gave the rate moves and other Fed actions a thumbs up.

The S&P 500 jumped 6.2% on the week and the other indices increased as well.

Following Far Behind

Left behind in all this – although still in the black – was the BDC sector.

BDCZ – the UBS Exchange Traded Note which owns most BDC stocks and which offers us sector data going back a long time – increased “only” 1.48%, after dropping (2.77%) the week before.

Still, 36 BDCs increased in price and only 9 decreased in this auspicious week.

Moreover, 9 BDCs jumped 3.0% or more – always a sign of some investor animal spirits.

3 BDCs dropped more than (3.0%).

Once Again

The biggest price loser in percentage terms was Great Elm (GECC), down (5.5%).

Last week, the troubled BDC had rallied off its lows, presumably on some enthusiasm for the new management and strategy just getting underway.

That enthusiasm diminished this week, but GECC is not yet back at its 52 week low as yet.

Underwhelmed

Also down was Logan Ridge Finance (LRFC) – off (4.39%).

The IVQ 2021 and year end results were disappointing with NAV Per Share down; losses at the operating level and no dividend resumption in sight.

As of Friday, the BDC trades at a (42%) discount to net book value per share, even as that bogey dropped (2.9%).

The discount is the largest one amongst the 46 market denizens we cover.

The market cap of what used to be Capitala Finance is a very modest $69mn.

Repayment Questions

The holders of the BDC’s three unsecured notes – two of which come to maturity in May – must be hoping to get repaid and get out before matters gets much worse.

No word yet, though, on how the two Baby Bonds with the tickers CPTAL and CPTAG get paid off.

Cash and availability under the Revolver are still insufficient – along with the need to finance every day operations – to repay those debts.

Will LRFC raise more unsecured debt to go along their existing 2026 notes, or increase their $25mn of secured borrowing capacity, or sell off more assets ?

On its most recent conference call, management seemed to be suggesting that increasing its secured borrowings to repay the obligations could do the trick, in an answer to an analyst on the subject:

Christopher Whitbread Patrick Nolan Ladenburg Thalmann & Co. Inc., Research Division – EVP of Equity Research

Great. And then given the current market conditions, do you really think you can lower your debt costs? I know you’ve got 2 debt issuances maturing in May.

Patrick Schafer Logan Ridge Finance Corporation – CIO

Yes. I mean, yes, I think we do. I mean, importantly, if you just kind of think about the existing structure, it’s entirely unsecured. There’s obviously a small — very small Keybank facilities undrawn that would be secured. So we think, at a minimum, swapping unsecured for secured borrowing should reduce our cost of capital without doing too much effort. So yes, we absolutely do think we can reduce the cost of capital.

Logan Ridge Finance- Conference Call Transcript – March 16, 2022

LRFC has $133mn of loan investments on its books. Of those $8mn are non performing and – typically – would not serve as valid collateral.

At a – say – 40% advance rate, LRFC could borrow up to $50mn on the back of a relatively diversified loan collateral base.

This could be supplied by KeyBank – the existing lender- or a new financier.

That $50mn and the cash on the balance sheet should be enough to meet the BDC’s immediate refinancing needs of $75mn, and leave a little something for running the business and modest AUM growth.

Less likely – but not impossible – is that both secured debt and more unsecured debt could be raised.

What happens in the next few weeks – after all May is just round the corner – will tell the story.

Big Bet

Also down this week is the perpetually volatile Newtek Business Services (NEWT), off (3.23%).

We hope the Board and management of the soon-to-be bank have not made a monumental misjudgment shedding their BDC cloak.

The stock is slightly down on a 1 week, 1 month, 6 months , YTD and 1 year basis after having the one of the biggest price run-ups in recent BDC history before the intention to change status came out.

Juicy distributions and ever stronger results have been insufficient to quell market doubts, but who knows what the future – and a different playing field – might bring ?

Where We Are Now

With the first quarter drawing to a close, and after much drama in the financial markets and great suffering in the Ukraine the BDC sector has essentially gone nowhere much in 2022.

BDCZ is down (0.5%) for the year while BIZD – the Van Eck exchange traded fund, which is very similar but in a different wrapper – is up 1.5% in the same period.

The number of BDCs trading up/flat or down in 2022 YTD : 20 to 26.

Also, the number BDCs trading within 5% of their 52 week high price – a favorite metric of ours – is 11. In the first week of January, the corresponding number was 12.

15 BDCs are trading at or above net book value, down from 18 at the end of 2021.

Impressive In A Way

All in all, nothing to write home about for BDC investors but considering that we’ve faced extreme inflationary conditions, a major European war; commodity shocks and now a promised campaign of higher short term rates with an uncertain time frame or outcome, a pretty auspicious outcome so far.

Admittedly, the gap between the performance of the BDC sector and the major indices has begun to narrow, as reflected in this week’s disparate rates of price jumps.

We remain in a transitory period by comparison with 2021. How the war in Ukraine plays out – and let’s be honest anything can happen in this regard – and with the struggle to tamp down inflation will weigh heavily on prices for some time to come.

This has been a volatile year where most stock and bond prices are concerned, and there’s no obvious end in sight even if the Fed has finally shown its cards – or at least some of them.

The BDC Reporter continues to believe that sector prices are more likely to move upward than downward for the rest of the year, especially if the Fed stays the course on rate increases.

In fact, we posit that if rates climb quickly, we may see a 10% or greater increase in BDCZ at some point.

On the other hand, the markets may already have taken into account the potential increase in earnings and dividend coming down the pike, but we don’t think so.

No More Dailies

By the way, we’re going to stop writing daily updates on what’s happening to BDC market prices. That focus certainly allows us to keep close track of changing conditions but is also very time consuming.

Instead, we’ll rely on these weekly Common Stock Market Recaps to keep readers updated on what’s happening to BDC prices, and focus more of our writings on providing ever more financial commentary and analysis about the 46 BDCs we track.

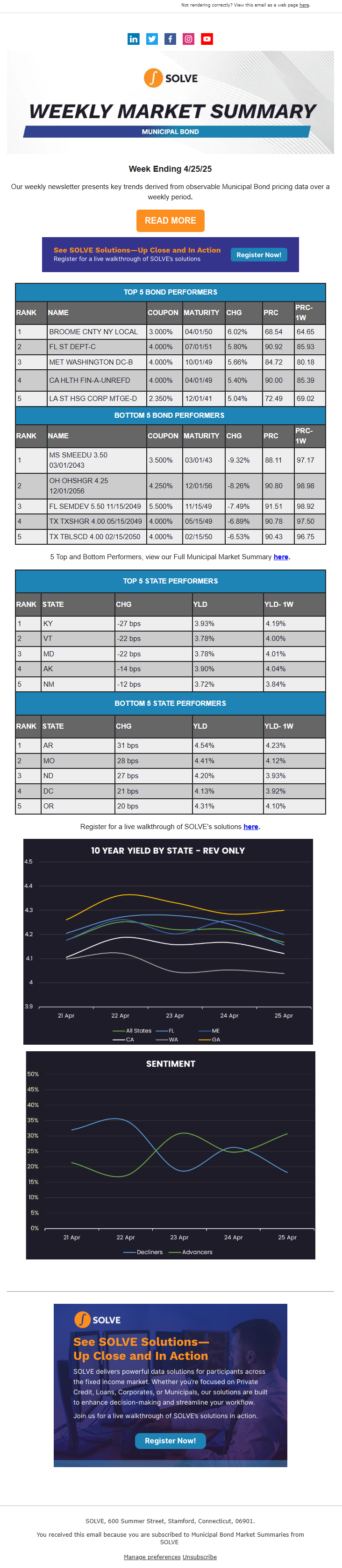

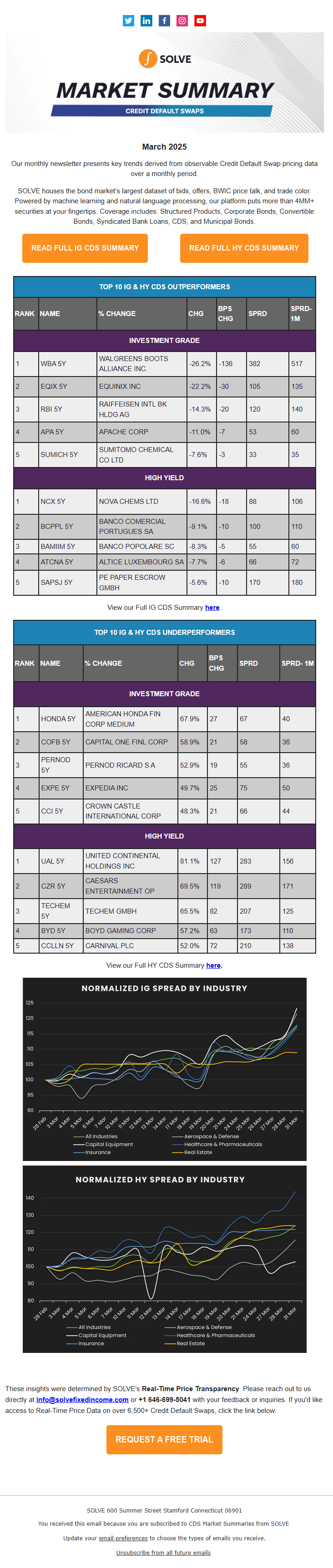

Syndicated Bank Loans

Syndicated Bank Loans  Municipals

Municipals  Corporates

Corporates  Credit Default Swaps

Credit Default Swaps  BDCs

BDCs  SOLVE Insights

SOLVE Insights  SOLVE Newsroom

SOLVE Newsroom